IA Fintech Member Insights: TOGGLE

Active Investing – A New Hope

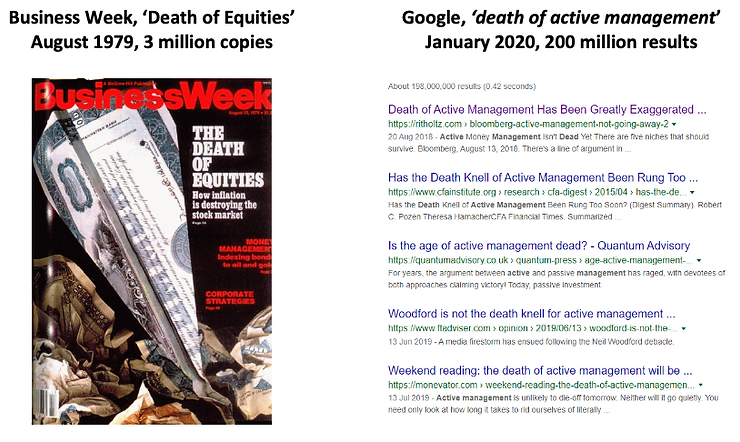

Arguments about the ‘death of active investing’ mirror stories about the ‘death of equities’ – which marked, in fact, the nadir for the asset class.

Musings about the death of active investing echo another famous prediction, BusinessWeek’s Death of Equities cover story, published on August 1979 – a few months before the start of the greatest equity bull market in history.

| Business Week, ‘Death of Equities’ August 1979, 3 million copies | Google, ‘death of active management’

January 2020, 200 million results |

Just like for equities in 1980, there are compelling arguments for a comeback in performance of active managers.

After a decade of underperformance, investors have meaningfully reduced exposure to active strategies

During the last decade active investors struggled – especially in equities – while any balanced allocation comfortably delivered Sharpe Ratios above 2x. Investors certainly responded to the differing performance between active and passive funds, leading to an epochal shift in asset allocations.

At the end of the decade, almost $ 3 trillion dollars shifted from active to passive strategies, with far-reaching impacts – while hedge funds shut down, semi-passive robo-advisors solutions captured almost $1.5 trillion in assets under management and asset management fees collapsed.

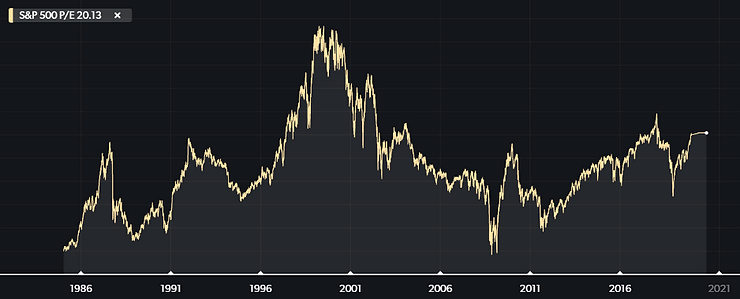

But with equity valuations close to historical highs tops and bond yields in the proximity of the zero bound, investors are looking again at active managers

From its ominous nadir in March 2009, the S&P 500 index rebounded five-fold and many global key benchmarks participated in its rally – German 10y Bunds pierced the zero bound, Bitcoin increased three thousand-fold from $5 to $15,000, and even rare watches saw their prices go up 200%.

Few investors would bet the next 10 years will experience a similar performance, and with nowhere to hide across asset classes allocators are looking around for alternatives and seek active management as a measure to mitigate downside risk.

Allocation to active managers is burdened by one key factor: performance

Issues with performance have been broad based, and trading oriented strategies failed to deliver just like fundamental equity investing.

As an example, after a stellar 300% performance from the late nineties to the crisis, CTAs and global macro funds lost on average 20% in the last decade even as markets posted a 5x performance. Equity strategies enjoyed a similar performance during the famous “value bull market” that lasted up until the crisis, only to fail subsequently.

It is hard to blame allocators under these circumstances for their change of tack.

The reasons for active managers’ underperformance remain a topic of debate – with QE winning the prize as the most-mentioned culprit…

At a conference in Geneva in 2015, an equity long-short Portfolio Manager on the speaker panel confided “It feels like in the last few years everything we’ve been taught about investing worked the other way…buy expensive, sell cheap, buy the news…you can’t fight against QE”.

With $20 trillions of liquidity injected in markets, and a deflationary wave adding downward pressure to yields globally, it is no surprise that asset class behaviours have changed in the last years.

However QE has for the time being paused and the investment environment might normalize going forward, even before balance sheet normalization begins. This will remove one headwind to active investors, especially those of a more fundamental and value-oriented persuasion.

…quant funds come as a close second…

Underperformance of active managers has been limited to discretionary managers, as quant funds kept gathering assets, reaching the $1tn mark towards the end of the decade. Some discretionary managers looked beyond QE and blamed quant competition for their underperformance.

Without doubt, competition by ‘flash boys’ funds has impacted discretionary managers in very-short-term trades, as depicted in Michael Lewis eponymous book – albeit investors are left puzzled when managers that market their “long-term investment style” but complain of competition from fast trading on earnings’ releases.

…and idea scarcity as a distant third

A third issue has plagued active managers across strategies, albeit without receiving the fanfare reserved for QE and Quant funds: “too much money chasing too few ideas”.

For many strategies, at any given moment there appear to be a small set of very popular ideas that grab the largest share of attention among market participants, and a review of 2020 outlooks by the top banks confirms the gut feeling: MS, Citi, HSBC, Goldman, JPM, and BAML. Commoditization of investment themes is a concrete problem – for managers, as much as for the allocators who pay fees for a commodity service.

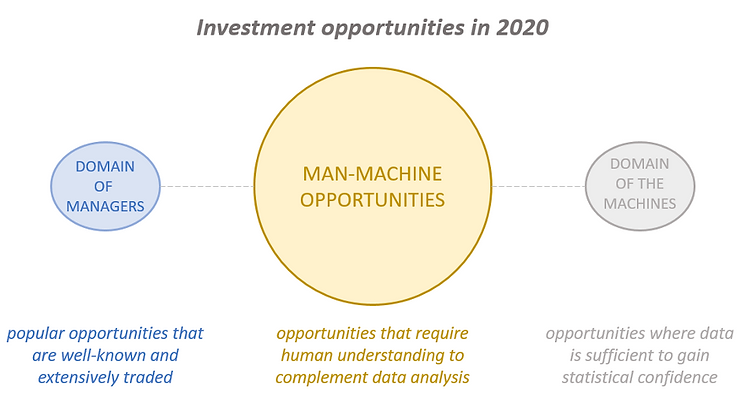

There remain large opportunities for active managers, beyond the scope of machines and consensus…

But whilst quant funds might have won the race for the “trading on news releases”, the jury is very much still out as to whether machines really spoiled longer term investing for fundamental managers.

In fact, opportunities abound outside of consensus and beyond the scope of machines, where data analysis and understanding complement each other. With the adoption of new tools, managers might discover more opportunities that fall outside of the common market narrative:

…and the technology and know-how for exploring these opportunities are finally entering investors’ toolkit

Even as legendary investment houses close shop and transition to family office status, forward-looking portfolio managers in their prime are opening up to the opportunities offered by AI and exploring new technologies for idea discovery and due diligence.

From tools that understand and summarize monetary policy decisions to full-fledged investment search engines, development of new-gen AI tools has led to better, more usable enterprise-grade software.

Slowly, investing applications have incorporated stronger capabilities along with a better understanding of how to engage users, taking the cue from consumer applications.

The opportunity for active managers is now

In conclusion, active managers stand now at the enviable position to capture massive inflows, as investors seek to inject a smarter and more defensive allocations in their portfolios. In many ways, this resembles the same opportunity captured by active funds after the first dot.com burst.

However, a lot has changed – more data, more investable assets, and a much greater weight of emerging markets.

Solving these challenges requires new tools, yet there is little doubt that those who succeed in building a working Man-Machine process will reap huge inflows in return.