Introducing a series on the Disruption of Capital Markets

Fast Tech, Slow Adoption

The previous article dove into the murky waters of the financial services’ stagnant infrastructure. We concluded that even though a large proportion of organizations face challenges when undergoing digital transformations, fortunately, the business and financial opportunities for those decisive enough are boundless.

This article marks the fourth installment of the series, “Capital Markets: Past, Present, and Future”, which covers the current challenges, the applicable technologies, and how some Fintech (Financial Technology) companies are harnessing the tides of change in capital markets today. It elaborates on the reasons why financial services firms have not been moving faster to upgrade their technology — leading to cost reductions, new revenue streams, and improved customer service.

Why is financial technology adoption so sluggish?

Banks and other capital markets participants have been investing in automation and Fintech startups over the past few years but the outcomes are still debatable. Below are some of the key reasons, reflecting multiple discussions with professionals in the industry — some with ex-colleagues and some not.

Growing by Accumulation

The larger banking institutions have grown primarily through the accumulation of smaller financial firms across the globe. As a result, they have inherited multiple, often redundant, and sometimes incompatible technology systems. Furthermore, these “silos” can be more than just digital — organizations may struggle to integrate teams and break down cultural, language, or other barriers inherent in acquisitions. Such challenges are not exclusive to the financial services industry, but that does not make them less real.

Organic Growth Turning into “Shoehorning”

Most large firms today have typically started small and at grew over time to become successful. In the beginning, firms utilize simple or bespoke IT systems that cover their limited needs. Growing fast, however, may lead to a situation where — in the interest of saving time and money — necessary IT upgrades/extensions get kicked further down the road or outright omitted. This eventually leads to new products being shoehorned into existing old systems, with “creative” patchwork and semi-manual processes. This “shoehorning” leads to a constant need for supervision and support or even worse, acceptance that relevant errors are a cost of doing business. Such outcomes are antithetical to the idea behind having IT systems.

The Lesser of Two (or Three) Evils

Whether they got here by acquisition or organic growth, many companies in the financial services are faced with a challenge. On one hand, challenges and security risks may surface when decommissioning legacy architecture with newer technology. On the other hand, preserving legacy IT puts hard limits on the obtainable benefits. It should come as no surprise that there still are systems in financial services firms that are almost impossible to integrate — the cost of doing so is seen as prohibitive unless it is a matter of life and death. The third option, outsourcing, is difficult — past client data breaches have had severe consequences from direct financial impact to reputational damage and churn. In such a highly regulated industry and in a context of heavy cost pressures, management tends to optimize for maintaining stasis, opposed to accepting the transformation process’ risks or a likelihood of an embarrassment.

Short-Termism and Politics — Safe Havens in Uncertain Times

Only blaming past choices for the sluggish adoption of financial technology is missing the forest for the trees. Legacy IT systems don’t run companies, people do..

A short-term outlook is a big barrier to lasting change. Companies may assume such a perspective during periods when the market, the economy or regulatory developments are hard to predict. At the same time, it is common for long-term strategic initiatives to face resistance from employees, even at senior levels. The new strategy can lead to restructuring, which leads to reduced team headcounts and even reduced personal gravitas within a firm. Research also points out that investors further exacerbate short-termism by their ever-shorter holding period of stocks. A short-term outlook introduces existential threats to financial services firms, particularly with the sheer volume of Fintech activity today.

Revolving Doors and Planning Cycles

Similar to politicians, business leaders often need to demonstrate progress and value generation within a short period of time; thus longer initiatives are often lost in translation. According to Equilar in a recently published post on the Harvard Law Forum on Corporate Governance and Financial Regulation, the average tenure of an S&P 500 CEO at the end of 2017 was only five years. This makes many CEOs focus on tactical results bearing fruit within their tenures, rather than long-term technology initiatives, even though they could objectively have a positive impact on the organization.

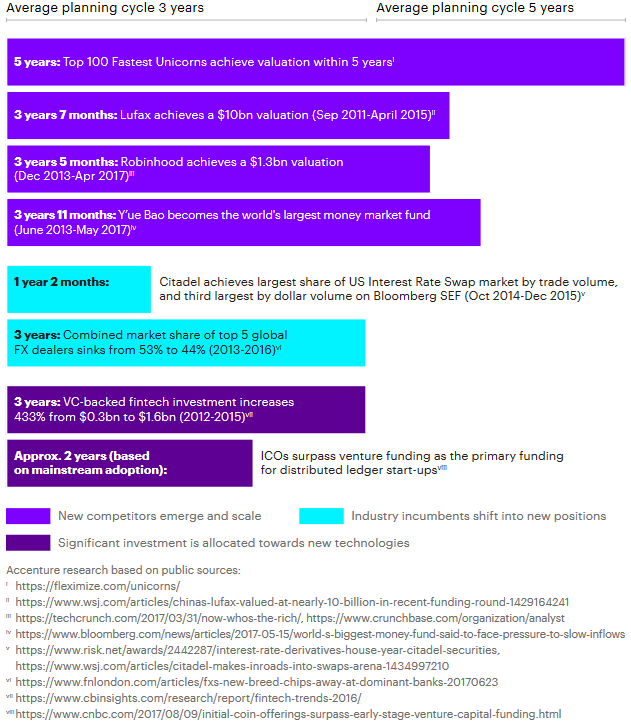

With the advent of Fintech however, the situation is not necessarily as gloomy as in the past. Accenture’s Capital Markets Technology 2022 report puts into perspective just how much could change within a financial firm’s typical strategic planning cycle. Technology is now enabling blazing-fast changes that can create or disrupt billion dollar companies and whole industries within only a matter of years.

Resistance to Change

Let’s say an organization overcomes the aforementioned hurdles to technology adoption and the required budgets are approved — negative results may still follow. First, there can be a disconnect between “tech people” and “product people” -the actual users- resulting in new technology solutions not always being well-thought out, making life more difficult rather and resulting in users reverting to the same old processes. Second, because of the slow adoption process, the “new” solution may already be outdated and not able to compete in the fast-paced technological landscape. It is no surprise that respondents in a recent report on perspectives of top executives highlighted their concerns about the overall organizational resistance to change and lack of willingness to make necessary adjustments to the business model and core operations, as factors which may affect their firm’s chances to survive these tectonic shifts.

The Importance of Digital Culture

Culture is a critical component when driving change. A recent study found that out of 40 companies examined, the 90% of those that fostered a digital culture sustained a strong or breakthrough performance (over the next three years). A comparable result wasn’t achieved by even one of those that neglected to work on their culture.

A minimum sustainable level of adoption of any emerging technology is required for lasting transformations to materialize in the financial services industry. Different institutions approach this topic differently, and it pleases me to know that some of the largest financial services firms we talk to at ResonanceX already have clear digital missions and are in the implementation phase. Most large players assume an approach which may look conservative but is cost-effective. They stay close to the more agile Fintech firms through collaborations, purchasing of minority equity stakes or by supporting them through entrepreneurship platforms. This places them first in line for either equity stake increases or buy-outs when such business model experiments (that’s what every startup is in reality) succeed by achieving scale and can be a Win-Win-Win for all — the industry, the startups, and the customers who are the ultimate beneficiaries of this tech adoption race. However, there is immense ground to be covered, in order to move the needle in the right direction.

In this series of articles, I cover the current challenges, the applicable technologies, and how some Fintech companies are harnessing these tides of change. Please share your comments and feedback as I explore these topics — from seasoned professionals, to technologists, to the eternally curious!

** The author, Dr Hariton Korizis, is co-founder of Velocity Innovator ResonanceX along with Guillame Chatain. The company is participating in the UK Investment Association’s Velocity Accelerator in London, and is regulated by the UK’s Financial Conduct Authority.