Author: Thread – threadlabs.co

Until a decade ago, most diligence processes conducted while creating investment theses were built on mostly financial analysis — an arbitrage between risk 🚫(debt, slowing growth, employee turnover, competitive pressures…) and reward ✅ (Company being Acquired, IPO, new market entrance, new product launch…). But that’s not the case anymore. As companies’ financial performance increasingly correlates with good management of extra-financial risks, investment professionals, are challenged to rethink the ways in which they evaluate a company and decide whether to invest.

A recent measure of performance that has been getting attention is Impact as an extra-financial element. Value-based investing, as a result of this, is an investment approach that looks at the environmental and social impact of a company’s actions, products, and leaders. While there is still isn’t a standard methodology around measuring this non-financial “value” or “impact”, the three most common approaches are — Impact Investing, Socially Responsible (SRI), and Environmental, Social & Governance (ESG).

In 2020, ESG-oriented investing accounted for $40.5 trillion in investments and is on track to exceed $53 trillion by 2025 (more than a third of the $140.5 trillion in projected total assets under management). The success of such ESG-focused investment approaches is often linked to cash flows in five important ways –

- facilitating top-line growth

- reducing costs

- minimizing regulatory and legal intervention

- increasing employee productivity, and

- optimizing investment and capital expenditures

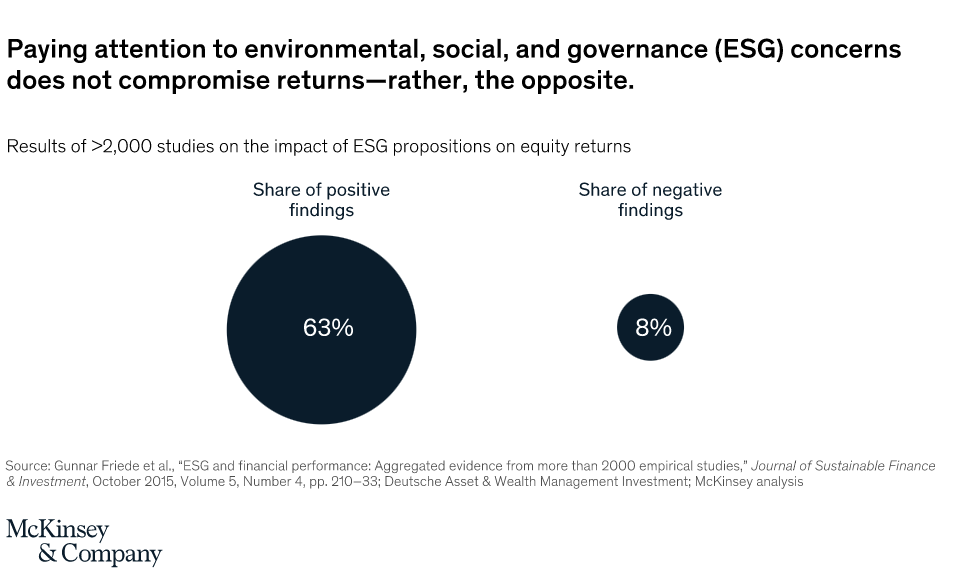

In 2020, the performance of Impact-oriented portfolios overwhelmingly met, even exceeded investor expectations for both impact and financial return, in investments spanning emerging markets, developed markets, and the market as a whole.

But, what’s keeping all investors from going all-in on sustainability?

It’s the difficulty in accessing data and the lack of a standard around sustainable investing.

ESG data comes in two main forms — raw data, mostly from Annual reports and ESG news, and refined data from ESG databases and broker reports. Investors then use this data to come up with a rating. For investors, scanning through annual reports of hundreds of companies is not just extremely time-consuming, but almost impossible. That’s why most investors look at ratings from agencies like MSCI, ISS, and Sustainanalytics, which rely on different methodologies that differ by their breadth of coverage (number of topics covered), or depth of expertise (eg. breaking down environment-related topics to different levels of granularity). It leads to confusing situations when an oil and gas company could be top-graded by one agency and poorly graded by another.

To comprehensively evaluate the extra-financial aspects of a company, investors generally focus on the following dimensions. Click here to learn more about the sustainability topics that matter the most.