Introducing a 10-part Series on the Disruption of Capital Markets

Implications of legacy infrastructure and fragmented processesss

The previous article looked at how financial services firms operate with fragmented and legacy infrastructure through the lifecycle of a Structured Investment*, a type of investment that carries a higher degree of complexity compared to stocks or funds, but offers better risk-return characteristics.

This article marks the third installment of the “Capital Markets: Past, Present, and Future” series, that covers the current challenges, the applicable technologies, and how some Fintech (Financial Technology) companies are harnessing the tides of change in capital markets today. It presents some of the important consequences resulting from the stagnant infrastructure used in financial services. So let’s dive into the murky waters to see just how these issues affect capital markets.

Reliance on manual processes

It is not a secret that a big part of the financial services industry is plagued by manual processes, reliance on paper documentation, and multi-channel client communications (e.g. emails, phone calls, text messages) that can all lead to errors, delays, high compliance risks, and require constant oversight. In some cases, there is still a need for manual human reconciliation of information between systems, when such systems just cannot be modified to communicate among each other.

A common reason is the rigidity of some of the current legacy IT systems, that makes them extremely hard to modify, or to interface with more modern systems, without introducing data security risks. This makes for a prime opportunity to deploy agile and flexible technologies, as long as they operate in a robust data-secure environment. A result of this is the tendency to prefer open architecture and open-source code, adopted across industries — the other end, where most firms currently are, is using bespoke, one-off systems, only to eventually realize that firms using them are captive by the vendor, their development resources bottlenecks and their pricing structure.

Reduced Profitability

A consistently high-cost base arises from the need to employ large operational teams or managing the regulatory requirements which are a chronic friction point for financial firms and their shareholders — weighing down on profitability and revenue growth. For larger businesses, this has a lesser effect due to economies of scale. Regardless, it forces them to limit activities to high revenue-generating market segments or transaction types, which could potentially lead them to exit from whole markets or businesses.

To put this in perspective and take an example from the Asset Management industry, when examining 153 leading firms in 43 markets representing $43 trillion (more than 62% of global assets under management), Boston Consulting Group found that in 2017, global profits decreased 2% as net revenues fell 1% and costs remained unchanged. This troubling fact is not a recent development and definitely not isolated in this particular part of the industry.

Missing out on the “data treasure trove”

It is a well-known fact that the amount of digital data generated by human activities is growing exponentially. When a firm does not have the right infrastructure, it becomes very hard to generate value from the extremely rich client activity information in its technology stack, which could improve the client experience and the firm’s profitability.

The historic approach of competing only in revenues, rather than catering for the client needs, is no longer working. This also led to reduced client engagement and increased risk of challenger startups incrementally capturing market share.

Even though banks and other financial services firms are aware of the immense value locked in their systems, it is costly and slow to leverage this value without replacing these systems completely, or without introducing risks from having external providers access and process client data.

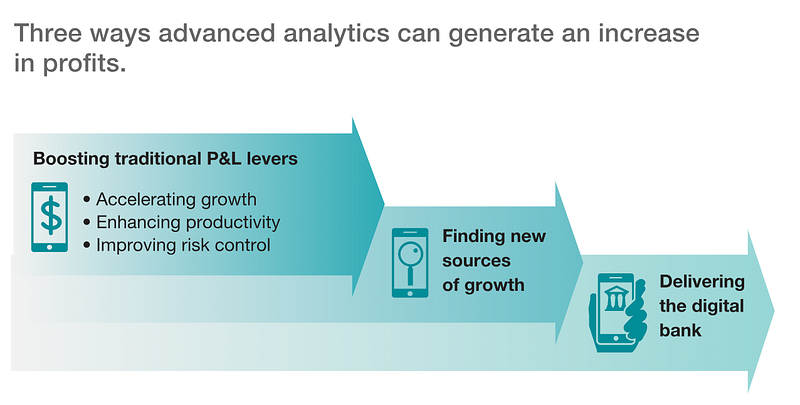

By embracing data, financial services firms cannot only significantly reduce fraud levels in real time (global card fraud alone is estimated to exceed $35 billion in 2020), but can also create customized experiences for clients by optimizing their transactional, investing, and behavioural interactions. The same data-led insights can also drive management decisions towards alignment to their key performance indicators and strategic vision. Below is a concise illustration provided by McKinsey of how data-informed analytics can provide significant value to financial services firms:

Complex and opaque transactions

The infrastructure relied upon by the financial system for the exchange of assets and money between trade counterparties is very scalable — indicatively, the Euroclear group settles over €733 trillion per annum of securities transactions. However, the way the global system is wired relies on a complex chain of intermediaries, and if something goes wrong (i.e. a submission of wrong information) it can be a headache to identify through the system where the problem lies — a needle in a haystack. Indicatively, most investment products are slow to clear and settle — typically taking between 2 days to 2 weeks to receive the proceeds from an investment via Euroclear / Clearstream in Europe or DTC in the United States. An improvement in the speed, cost, and transparency in the “plumbing” layers of the financial system is dearly needed.

Subpar client experience

Low engagement levels for the different generations of investors will make some firms miss out on the monumental $30 trillion in generational wealth transfer that will happen over the next decades.

If they cannot keep up with the large changes in terms of mobile and social habits, how are they going to keep clients from switching to more engaging financial services firms, or becoming disengaged by platforms that cannot service their rapidly growing needs with a high enough degree of personalisation?

How do you service clients, now used to checking their mobile phones within 15 minutes of waking (along with other trends and challenges of the younger demographics)? Gone will be the days of meeting with your Financial Advisor for a quarterly review – they are being replaced with a more direct, opt-in interactivity where clients have full and real-time information and can engage with questions, as long as they have an internet connection.

Accelerating rate of change

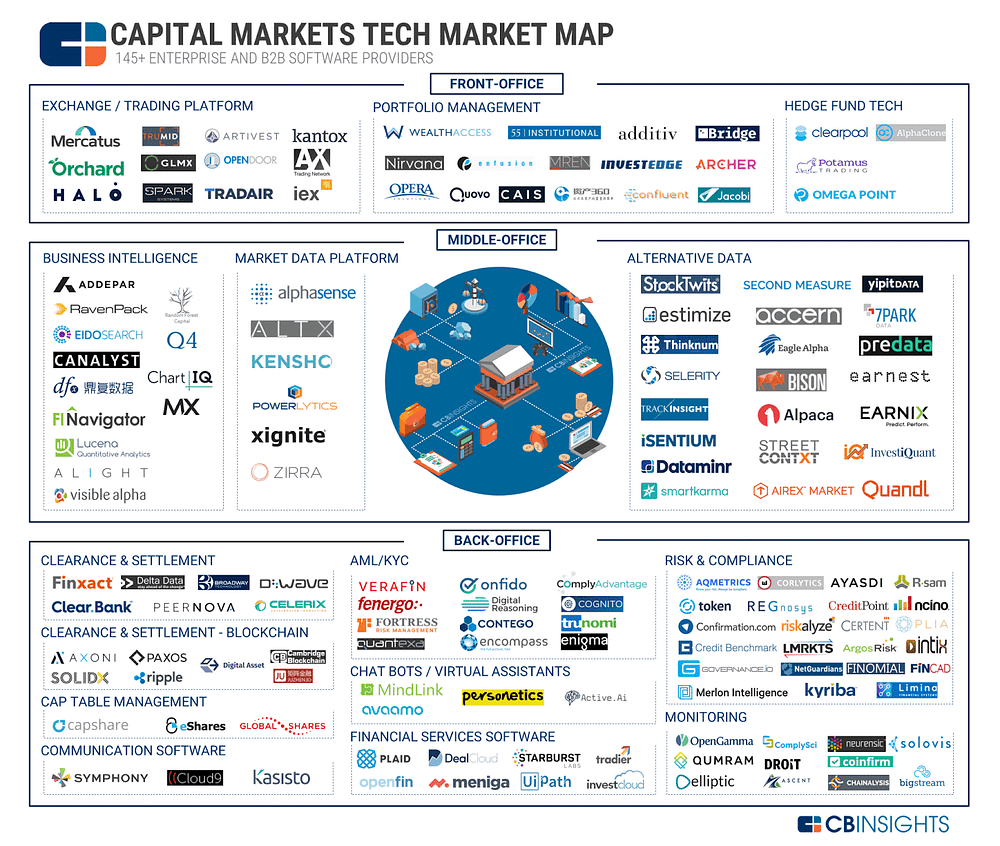

The tempo of innovation is accelerating. Institutions with a high degree of bureaucracy and low degree of adaptability will be finding it increasingly harder to modify the business model fast enough or deploy the right forward-looking partnerships – neither of which are core capabilities of traditional financial firms. In contrast, more agile Fintechs able to collaborate with the wider ecosystem can cheaply deploy and cheaply new and potentially disruptive propositions. One by one, these agile startups will become more able to isolate and improve upon core functions of banks, changing the whole financial and investing landscape as we know it. To get an idea of just how large this space has become, below is a recent map of the ecosystem.

Summing up, it is no surprise that according to a recent industry report 42% of the organisations surveyed cite legacy infrastructure and systems among the three top challenges to digital transformation (the other two being customer experience and business efficiency), and that 80% of firms that now undertake digital transformation initiatives expect to lose revenue in the 12 months, if they do not succeed. Fortunately, the opportunities arising are boundless and firms able to implement elegant and robust customer-centric capital markets architecture do not only stand to benefit the most, but will also be the leaders of positive impact to society as a whole.

* Structured Investments are investment solutions of fixed maturity, expressing an exposure to a bond and a derivative, packaged in a singlesecuritized product. Typically, they are traded through notes or certificates.

** The author, Dr Hariton Korizis, is co-founder of Velocity Innovator ResonanceX along with Guillame Chatain. The company is participating in the UK Investment Association’s Velocity Accelerator in London, and is regulated by the UK’s Financial Conduct Authority.