Introducing a series on the Disruption of Capital Markets

This article is the second installment of the “Capital Markets: Past, Present, and Future” series, that covers the current challenges, the applicable technologies, and how some Fintech (Financial Technology) companies are harnessing the tides of change.

The previous article presented the thesis that after decades of insufficient and unbalanced technology adoption in the financial services industry, capital flows to Fintech have substantially increased to remedy the problem. Such conditions are rarely not a preamble of significant developments.

Even though every aspect of our lives has been affected by the huge technological leaps of the past two decades, the finance industry has remained relatively stagnant.

Technology can greatly simplify the investment process — making it cheaper, faster, and safer. It opens up more opportunities for agile firms to compete and innovate, while the end investors can receive the best possible service. Although it is tempting to dive right into the solutions, it is imperative to first intimately understand the problems.

The Challenge

At a high level, the challenge is that most of the technological systems and tools aren’t capable of managing all the inherent complexities of “interactions” between investors and financial services firms (e.g. exchanging money and assets during the investment process). Automation so far has enabled quick and cheap access to investments at the lower end of the complexity spectrum (e.g. stocks, and Exchange-Traded Funds). It has yet to enable other forms of investments with potentially more beneficial risk-return characteristics (e.g. Structured Investments*). Considering the full lifecycle of investment solutions — from their manufacture to issuance, marketing to distribution, events management (e.g. investors receiving an annual return on their investment) to post-trade analytics (i.e. investors having a good understanding of relevant performance) — such compounding complexity results in multiple risks and high enterprise-wide risk management overheads. Furthermore, any such infrastructure is required to ensure that legal and regulatory requirements are met at every step of the way. If this doesn’t feel onerous enough to you yet, this infrastructure also needs to be flexible to adapt to the ever-changing technological, legal, and regulatory landscape across the globe. Adaptability is key in allowing companies to be agile in adding new business lines and innovative products.

The consequence is a need for manual or semi-automatic tasks that add to the risks, delays or uncertainty already inherent in the investment process. Have you ever labeled an email as “Urgent”, only to receive an “Out-of-office: I’ll be in Cancun for my 2-week holiday” response? I am not talking exclusively about deeply technical issues or mundane operational processes; emails are part of the financial services infrastructure too, and every part of the process is just as important as the next.

Recounting the Complexity

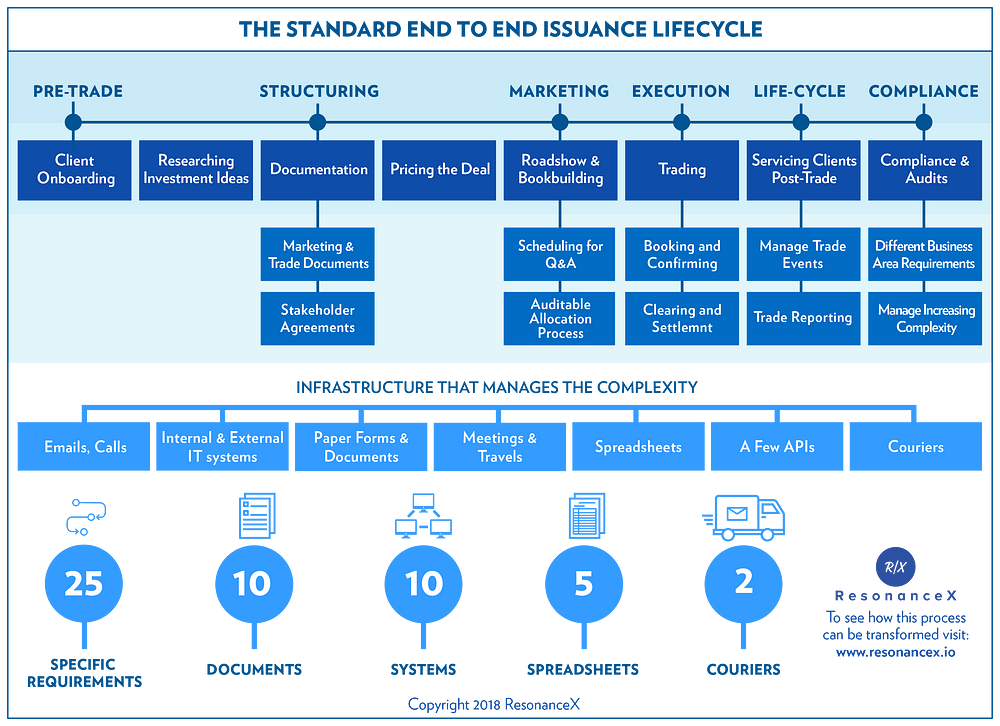

But, let’s start being specific. As an illustration of the complexity and risks that are managed on a daily basis, let’s focus on the full lifecycle of a Structured Investment solution. A popular distribution method for such products is the Private Placement, typically involving the sale of securities to a relatively small number of select investors. The steps differ (depending on the type of investment, the jurisdiction, the sophistication, and the degree of automation linking the manufacturer with the investor) but the complexity is typically high and ever evolving. A Private Placement process typically involves the following elements, broken down into three buckets: i) more than ten documents or forms that need drafting, agreement, possible negotiation and signatures, ii) the synchronization of at least ten typically fragmented IT systems (e.g. internal and external communications, pricing, risk management, settlement, etc.), and iii) using at least five different internal records or spreadsheets (e.g. keeping track of clients, investments, fees, etc.).

This “infrastructure” may also include courier services in jurisdictions where the law requires hand-signed documents stored in secure document depositories, rather than accepting digital signatures.

The graph below provides a run-through of the steps as well as the infrastructure elements, typical for manufacturers (from the smallest to the largest) of such structured investment solutions.

While the above is still an oversimplification, it’s not hard to see how the process is just short of a labyrinth. While this complexity is not limited to structured investments, these financial products stand to benefit significantly from the expert application of technology.

The Way Forward

Summing up, financial services firms engaged in Capital Markets do use platforms and tools to tackle the aforementioned complexities, some being advanced too. IT infrastructure, however, remains typically fragmented (some even built across different decades). It can be hard or impossible to upgrade, which requires custom-built spreadsheets and human procedures, oversight, and reconciliations, even in the most advanced of operations.

The Structured Investments space exemplifies that the challenge does not necessarily lie in the lack of tools, but in the rarity of what we could describe as an efficient holistic architecture for the creation, compliant distribution, education, and investment in such solutions.

Next week I’ll be taking a closer look at some of the adverse implications of such fragmented and legacy processes within financial services. Stay tuned!

* Structured Investments are investment solutions of fixed maturity, expressing an exposure to a bond and a derivative, packaged in a single securitised product. Typically, they are traded through notes or certificates.

** The author, Dr Hariton Korizis, is co-founder of Velocity Innovator ResonanceX along with Guillame Chatain. The company is participating in the UK Investment Association’s Velocity Accelerator in London, and is regulated by the UK’s Financial Conduct Authority.